Model Objective

- Proprietary quantitative, rules-based methodology that makes a “probabilistic” determination of risk of loss for each ETF.

- Developed over a 16-year period.

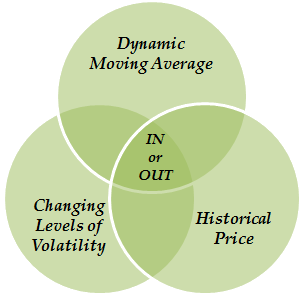

Key Inputs to the Model

Output from the Model

- The RPg Tactical methodology determines a forecasted performance relative to cash returns.

- Results in a sector either included, or removed from the portfolio entirely

Tactical U.S. Equity Process

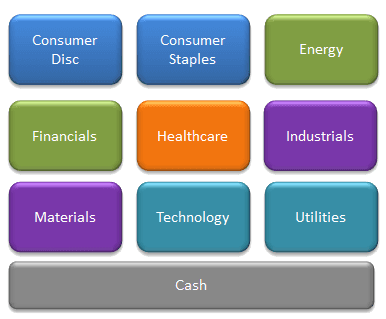

Investments Include

- Nine of the 10 major sectors of the S&P 500.

- Cash and or cash equivalents (used during bear markets).

Positions are evaluated on a weekly basis

Sector ETFs are traded using a disciplined rules-based methodology

- U.S equity exposures diversified across the major U.S. sectors.

- Implemented through liquid ETFs to enhance transparency and efficiency.

Sector position weighting for sectors remaining IN the portfolio are always equal weighted at the time of rebalancing

- There is a maximum cap of 25% for any sector ETF at time of rebalance.

- Final sector ETF weighting is determined after going through the ActiveParadigm process.

When 6 or more sectors are removed, the ActiveParadigm methodology will begin to raise cash

- When 3 sectors are IN, the portfolio will have 25% in cash; 2 sectors IN = 50% cash; 1 sector IN = 75% cash.

- Portfolio may have 100% in Cash & cash equivalents.